If you haven’t heard, President Obama signed a new tax bill last week. One of the items that will affect all employees is the 2% point reduction in an employee’s share of Social Security portion of the FICA Tax, from 6.2% to 4.2%. What exactly does that mean for you?

The table below illustrates the change and savings. FICA limits are currently adjusted for inflation and are currently set at $106,800. The tax savings is currently only available for 2011.

Pay 2010 Tax (6.2%) 2011 Tax (4.2%) Savings

$30,000 $1,860 $1,260 $600

$50,000 $3,100 $2,100 $1,000

$80,000 $4,960 $3,360 $1,600

$100,000 $6,200 $4,200 $2,000

$106,800 $6,621 $4,485 $2,136

This is a huge opportunity for every employed person to increase their 401k contributions or contribute to an IRA or a Roth IRA in 2011. This is FREE money, folks. Using it for retirement is a very wise move.

Please call me if you need more information or want to take advantage of the extra money in your pocket by smart retirement investing.

Wednesday, December 22, 2010

Monday, December 13, 2010

2010's Big Tax Bill Explained (Part 1)

13 pages of summaries are what comprises the new Tax Relief, Unemployment Insurance Reauthorization and Job Creation Act of 2010.

My daunting task, should I accept it (and let's face it, I am accepting it because I'm writing this), was to wade through the jargon to find what would be useful to the average tax payer, like you and me.

There are 7 main parts to this bill, but today we are covering what's just under the first section called the "Temporary Extension of Tax Relief."

What's found in this section of the bill is a lot of tax break extensions from 2001 and 2003 that were set to expire, but are being extended through 2012. (You may feel some deja vu, but this is what the American Recovery and Reinvestment Act did last year for 2009 as well.)

The bill...

· Continues the reduction in income tax brackets for 10%, 25%, 28%, 33% and 35%

· Extends the capital gains and dividend rates

· Increased extension of credit from $500 to $1000 for the Child Tax Credit

· Extends the marriage penalty relief

· Gives incentives for families and children

o Expanded tax credit for child care costs for children under 13 and special needs dependents

o Tax credits for qualified adoption expenses

o Tax breaks for employers purchasing or building a child care facility for their employees

o Continuing the 45% tax credit for working families' first $12,570 worth of income

· Education incentives for those going to school

o Coverdell savings accounts remain tax exempt

o Employee can exclude up to $5,250 worth of income for employer provided education assistance

o Student loan interest deduction up to $2,500

o Excludes scholarships from income

· Bond exclusion

· American Opportunity Tax Credit extended (Rebate of up to $2,500 of tuition or education related expenses)

Bookmark this post: |

|

Monday, November 22, 2010

Top 10 Financial Tips for Newlyweds

My dear niece is getting married in March, 2011, to a wonderful young man. As I have been thinking of this wedding and the two wonderful people that will be starting a life together, I cannot help but think of the financial advice that I can offer them so they can have a prosperous life together.

Here are the top ten ways to keep financially sane, today and for the rest of your life together:

- The power of compounding interest is truly a miraculous thing but it takes time. Start saving now when you have nothing but time ahead of you and your money will grow exponentially.

- Always save 10% of your income—each and every year—no exceptions.

- Go slow on large purchases and always consult with each other. Set a dollar limit that each can spend on his/her own.

- Avoid credit card debt like the plague. Only charge what you can pay off when you get your monthly statement.

- Have money set aside for emergencies and believe me, they will happen. A rule of thumb is approximately 3 months of your monthly earnings.

- Be generous. Sit down together and decide what annual amounts you want to give your church or charities so that others can be blessed.

- Contribute to your employer retirement plans so that you always get the match. If your employer has no plan or no match, consider contributing to an IRA or a Roth IRA. Remember… compounding interest is phenomenal.

- Buy term life insurance only. Check with your employer about group term life, it is almost always the cheapest way to go.

- If you are having trouble with more expenses than income, seriously look at cutting out the extras such as expensive cell phone plans, cable TV, eating out etc… Taking lunches to work saves a lot of money!

And, of course, number 10...

10. Seek the wise counsel of your Aunt Judy. She knows what she is talking about!

Bookmark this post: |

|

Tuesday, October 12, 2010

Journey to Haiti (Part 2)

It has been only been three weeks from my experience in Haiti...The devastation and hopelessness that I witnessed will haunt me forever. However, I left a big chunk of my heart in Haiti and know that someday I will return. I pray for world leaders to unite and truly help Haiti become a viable country with exports and manufacturing.

The people are willing—they want to work and have a better life. They don’t need money to be dumped into the country…they need education and training and jobs that they can perform. They need dignity and empowerment. Haiti desperately needs leaders to rise up who care only about Haiti and how to make it better and not their own selfish ambitions. The Non Government Agencies (NGO’s) and churches of all faiths are the hope of Haiti. These are the people who truly care about the beautiful and resilient Haitian people.

I am so proud of my church, Generation in Oceanside that is going back to Haiti for two more trips in 2011 to help a local church expand in size and thereby be a blessing to more people in the community that it serves. This church currently cares for 20 orphans that lost their parent(s) in the earthquake. I personally met each one of these children and each child is imprinted on my heart forever. They will be taken care of and educated by Pastor Pierre’s church until they are self sufficient. They are the Hope of Haiti.

These photos are courtesy of Jonathan Moyer. We invite you to explore his Haiti Photo Gallery. Thank you, Jonathan!

Bookmark this post: |

|

Monday, October 11, 2010

Top Five Year End Tax Saving Strategies

We are only two and a half months away from 2011! Some families are realizing that they do not have a lot of time to enact some tax savings before the year is out. We're here to help! It appears that 2011 is headed for higher taxes, below are the top five ways to do some tax saving before the year is over:

1. Sell stock. A smart tax strategy is to sell some highly appreciated stock/stock funds before the end of the year and pay capital gains at the lower rates in 2010. Often, the tax bite can be mitigated by also selling some of your “losers” at the same time, thereby offsetting some of the gains with the losses.

2. Charitable giving. Charitable giving is always a great way to save on taxes and do some good! Gifting appreciated stocks to your favorite charity(s) is also a great tax savings tool. The charity gets the fair market value of the stock transferred and you get the tax deduction and it saves you the capital gains taxes.

3. Tax sheltered giving. Tax sheltered plans are one of the best gifts that Uncle Sam has ever given us. A person 50 and older can defer $22,000 into his/her 401k, 403b, and 457 plans for 2010 and everyone else can defer $16,500. This results in significant tax savings for you, the investor. Check your current pay slip and see how much you are on track to contribute for 2010. If you will not meet the above maximums, ask your HR department to increase the monthly amount so that you can take advantage of these limits and save BIG on taxes.

4. Invest in a Roth Conversion. Roth conversions are in the news this year. For the first time ever, folks making $100,000 or more can covert their traditional IRAs to Roths this year. Yes, taxes will be due on the converted money but Uncle Sam has also given us another nice gift. You can pay the taxes over a 2 year period. That really helps take the sting out of the tax bite. An interesting provision in the recently signed Small Business Bill is that employer tax sheltered plans can now allow their employees to do Roth Conversions of their 401k, 403b and 457 plans. If this is of interest to you, check with your HR department for the details.

5. 2010 Tax Energy Credits. The personal energy tax credits expire at the end of 2010. If you are planning on getting more energy efficient windows and/or doors or installing heating or cooling units, then please do so before the end of 2010 and get up to 30% of the purchase price as a tax credit for the year. Credit tops out at a generous $1500.

Please feel free to contact us for more information if you need any more information or assistance on how to implement any of these tax savings strategies.

Bookmark this post: |

|

Monday, September 20, 2010

Journey to Haiti (Part 1)

Hello everyone! This is Marcie filling in for Judy today. As some of you may know, Judy has taken some time this week to visit Haiti with her church, Generation Church. This trip is a scouting mission trip of sorts, to see where Generation Church can make an impact in the rebuilding of Haiti. So far, it has been a strenuous and hard trip. Phone calls and texts are hard to come by, so the team has been emailing and posting thoughts and photos to Facebook. Below are some words that Judy sent to her family.

{kind=link}

This is indeed a tough trip. The sights are so overwhelming. People living like this are beyond words. The people are so resilient. All kinds of tents set up everywhere --they sleep in there at night and may work out of their shack/homes during the day. But they are so scared to be indoors at night. The wreckage is hard to describe. It just doesn't seem like much has been done.

|

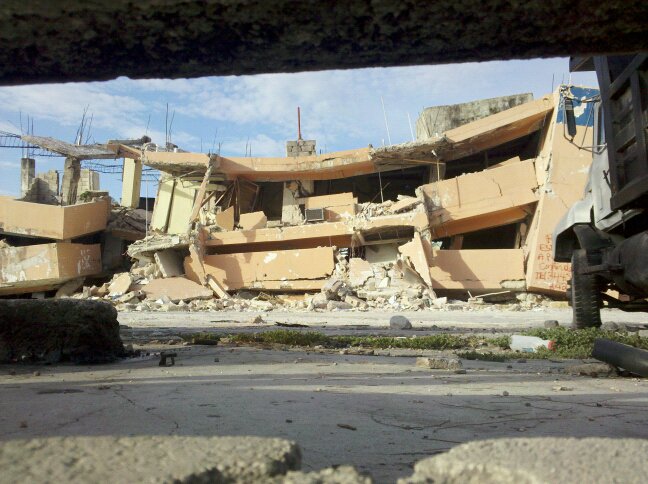

| Supermarket collapse in Haiti |

{kind=link}

Today is Sunday and we arrived at Pastor Pierre's church at 8:30am and left around 2:00pm. Church and worship lasted over 3 hours in a small room filled with people (crammed in) and only a few fans. Pastor Pierre is a small man--very rotund--with a booming voice and infectious joyful personality. We loved him and his wife and 10 children. They live in a small area over the church--7 boys in one bedroom probably half the size of one of our bedrooms and the 3 girls in with the parents. Church was filled with songs and clapping and preaching and joyful praising. One of the most memorable church services I have ever been to. Shawn preached and of course, we had a translator.

|

| Pastor Pierre and his family |

Daybreak and Generation Church are going to talk about sending construction teams to expand the church building for him. He has an opportunity to buy the three rooms attached. Trust me--it needs to be bigger!!! It is absolutely stifling here and very little water pressure. Showers are a trickle. Tomorrow, we go and visit the 20 orphan kids that Pierre's church is taking care of.

|

| Church in Haiti - needs to be bigger! |

All I can do to get past this overwhelming hopelessness is to know that 20 kids are being cared for, educated and loved and will grow up to be a light in this part of the world. And that Pastor Pierre can make a difference in his community thru his church and be a light. If I cannot cling to this and focus on it--I would be overcome with despair."

We will have more thoughts and photos, hopefully today, depending on the availability of the Internet, of course. Thank you for reading and your continued support. Please feel free to comment below, I will send any comments to Judy via our next corresponding email.

Bookmark this post: |

|

Friday, July 30, 2010

Thoughts from Atlanta

I am blogging from Atlanta while attending the NAPFA (National Assn Personal Financial Advisors) Core Competency Conference. This morning we had an excellent speaker from the Atlanta Federal Reserve named Michael Hammill. I will share with you some of the key ideas that I gleaned from his presentation:

- We are in a period of moderate economic growth (about 2.5%) since the first quarter of 2010. While this is not a great number, at least we are moving in the right direction

- Consumer confidence is fairly pessimistic which translates to weak consumer spending. Since consumer spending is 70% of GDP growth, you can see how this translates to the slow growth numbers cited above. Wages drive consumer spending and when you consider the number of people unemployed or underemployed, it makes perfectly good sense that people are not spending because they cannot spend. And the savings rate is up sharply. When we went into this recesssion, the savings rate was negative. It is now hovering around 7%. As a financial planner who preaches a 10% savings rate for people, this makes me very happy. Although the paradox is that we need people to spend in order to grow our economy.

- Unemployment is around 9%. However when you factor in the number of people who are underemployed (working part time instead of full time) and the folks who are so discouraged that they have actively stopped looking for work, this number should be doubled. So, the TRUE unemployment rate is more like 18%. Ouch! We are adding about 100,000 jobs a month but when you consider that we were shedding more than 800,000 jobs a month during the recession (depression?), it will take us 5 more years to get back to pre-recession job growth.

- Business inventory levels are growing --a good thing!

- Housing market is very poor. It was propped up with the generous tax credits but those have all expired. The forecast is that housing market will remain very weak for the next four years. It will take until 2012 to work thru the short sales and foreclosures clogging the market. And until 2014 before housing prices start to rise. Bad news for people trying to sell their home. Hardest hit areas are Florida, Calif, Nevada and Phoenix--the sunshine states where the biggest bubbles were. No surprise there.

- Inflation not expected to be an issue for several years--good news

- Financial markets adjusting to a new normal--stricter credit --weak loan demand. Loan defaults (except for real estate) have peaked and are now declining.

- Europe is working through their debt issues and not as much effect on US markets as expected.

Bookmark this post: |

|

Monday, July 26, 2010

New Financial Reform Bill: Progress Or Not?

If you have turned on the news, you probably have heard and re-heard reports on two events: the horrendous BP oil spill and the, newly passed, Financial Reform Bill. While I wish I had insight on how to fix the oil spill, I do have a few thoughts about the Reform Bill that was passed Thursday, July 15th.

So, what is in this Reform Bill?

Jill Schlesinger, author of "The Financial Decoder," and contributor to CBS' Moneywatch.com, wrote an article on June 25th, using with layman's terms, what the bill can and cannot do. She states, "the bill probably won't prevent the next crisis," but it will help consumers in some ways.

For example, there will be a new Consumer Financial Protection Bureau, which will help consumers by moderating the credit card and house mortgage industries. According to the Senate, the new Bureau will "finally [be] a watchdog to oversee financial products, giving Americans confidence that there is a system in place that works for them – not just big banks on Wall Street."

Schlesinger says in another article about the new Bureau, "The new rules will prohibit mortgage brokers from steering customers into more expensive loans for a commission and will ban no-documentation or "liar" loans. It will also make credit card statements more readable and transparent, allowing consumers to more easily compare products."

She also notes where the new Bureau will not protect consumers in all things, namely auto dealer supervision and addressing the fiduciary standard: "Although the new consumer rules are a step forward, there are some noticeable omissions. During negotiations, two important consumer measures were left out: the oversight of auto dealers and the fiduciary standard. I'm particularly upset about the later, which would have made it law for financial professionals to put their customers' interests first."

I agree with Schlesinger about these omissions, namely about the fiduciary standard. We work very hard at Stewart Financial Services to address our client's needs first. There are many planners and institutions out there who base their financial advice simply on what funds would give them the biggest commission, or return... regardless if it's a good fit for their client's financial goals or dreams.

The SEC has been delegated to take care of an umbrella fiduciary standard for all financial advisors. We hope to see progress on this front, hopefully, within 6 months from now.

If you have a question about what the fiduciary standard is, please click on the orange button below. Stewart Financial Services is proud to follow all these guidelines for our clients' financial well being.

|

| FocusonFiduciary.com |

Also, if you have further questions about the Financial Bill Reform, you can click here to view Senate.gov's complete copy of the bill, or, as always, feel free to ask me. I feel the Consumer Financial Protection Bureau is a good step in the right direction... let's just keep making these steps!

Bookmark this post: |

|

Sunday, July 11, 2010

The Really Important Things in Life

Yesterday my daughter and I attended a wedding in our old neighborhood. We moved away from that home and our dear neighbors next door some 24 years ago. The sweet daughter of that family was the beautiful bride yesterday. Even though many years and "much life" has passed in those 24 years, we felt like we were with family all day and we were so honored to be part of their special day. We even got to tour the backyard of the house that we lived in for 12 years. The house where my daughter lived for the first 4 years of her life. Lots of good memories made in our home and the home next door. And the time and distance between us was like it never happened. We felt loved and part of their circle.

So...why is my personal finance blog reminiscing about the good old days? Shouldn't I be talking about investments, rate of returns etc....? Because yesterday helped me reflect on what is truly important in life. For me, it's spending time with my family and dear friends, gazing at the amazing milky way in Borrego Springs with my husband, walking my dog at the beach, brushing my kitty (she is deliriously happy when I brush her), getting lost in a book for hours, going to Padres baseball games, planning our upcoming missions trip to Haiti, shopping for a bridal dress with my niece and family, cooking and planning healthy dinners. I could go on and on.

For my clients, I strive to help them figure out "how much is enough". So that they can spend their time on the things that are really important in their lives. Oh...and working with my clients... is one of the truly important and fulfilling things in my life.

So...why is my personal finance blog reminiscing about the good old days? Shouldn't I be talking about investments, rate of returns etc....? Because yesterday helped me reflect on what is truly important in life. For me, it's spending time with my family and dear friends, gazing at the amazing milky way in Borrego Springs with my husband, walking my dog at the beach, brushing my kitty (she is deliriously happy when I brush her), getting lost in a book for hours, going to Padres baseball games, planning our upcoming missions trip to Haiti, shopping for a bridal dress with my niece and family, cooking and planning healthy dinners. I could go on and on.

For my clients, I strive to help them figure out "how much is enough". So that they can spend their time on the things that are really important in their lives. Oh...and working with my clients... is one of the truly important and fulfilling things in my life.

Bookmark this post: |

|

Monday, June 28, 2010

How To Spot and Stop Senior Financial Exploitation

I read a recent article in the Los Angeles Times and was reminded, even more, of why continual vigilance is needed for senior financial exploitation. This chord strikes close to me as I have an aging mother and do worry from time to time how she could be approached for senior financial abuse.

Senior financial abuse doesn't seem to make headlines on CNN, but it is very prevalent. I was surprised to see some of these statistics in a recent survey done by these organizations: the North American Securities Administrators Association (NASAA), Investor Protection Trust, and the National Adult Protective Services Association (NAPSA).

Here are some surprising statistics from their survey:

• Half of older Americans exhibit one or more of the warning signs of current financial victimization.

• Almost half of those aged 65 or over (44 percent) got at least two out of four questions wrong about basic investment knowledge.

• About one out of three older Americans (31 percent) says they are vulnerable in one or more ways to potential financial victimization.

• Only 5 percent of adult children in touch with their parents' doctors report "the healthcare providers ever mention[ing] any concerns about your parents handling of money or relayed any concern from your parent about handling money." Only 2 percent of Americans aged 65 or older say that their healthcare provider has ever asked about "how you are handling money issues or problems."

• Four out of 10 children of parents 65 or older are "very" or "somewhat" worried that their parents "have already become or will become less able to handle their personal finances over time."

Half of our seniors exhibit warning signs of financial exploitation? Sounds scary, doesn't it? I am relieved that there are some who have heeded the warning signs and are taking action. The NASAA, Investor Protection Trust, and the NAPSA, along with medical professionals and social workers, are banning together to create the Elder Investment Fraud and Financial Exploitation project, whose sole job is to stop a "rising tide of economic exploitation of the elderly." (Kristof, LA Times)

But what can the average person do right now to prevent senior financial exploitation? The California Society of CPA's recommends that the best defense is a good offense:

• Be aware – it can happen to your family

• Identify vulnerabilities

• Take action to safeguard your family

• Look for clues of abuse

• Take action if you suspect fraud

Sheryl Rowling of Advisors4Advisors further explains what that action can look like:

“Financial fraud can occur in small amounts over time. For seniors on a fixed income, even $10 here and $20 there can be devastating. The most common scams against seniors fall into three groups:

• Telemarketing scams: More than a third of telemarketing fraud victims are over 60 years old. The most common scams are free vacations packages, time shares, sweepstakes, phony charity fund raisers, and expensive 900 numbers.

• "Free" lunch investment seminars: Shady financial advisers often lure seniors to a free lunch or dinner, promising advice on “senior” issues such as living trusts or estate planning. Once there, seniors are pressured into purchasing dubious investments such as annuities or promissory notes. Although technically legal, these products are monumentally bad choices for retirees - illiquid, complicated and booby-trapped with high fees.

• Religious or social group fraud: Among con artists' favorite targets are members close knit religious or social groups. The con joins the group and then tries to sell fraudulent investment schemes to members.

One of the easiest - and most effective - ways to protect parents is to talk to them about the common financial scams. Tell them it's important they know what's happening - if for no other reason than to warn their friends.

Also, it's important that children know their parents' social circle. Are they mentioning a new name? Have they begun to talk about someone that has "a lot of good ideas" about money? Children should introduce themselves to new people entering their parents' life. Con artists are looking for easy marks, not people with family or friends looking out for them.

Theft committed by a caregiver, such as a nurse or aide, can be very difficult to uncover. There are warning signs of caregiver financial abuse. Watch for signs that a caregiver is trying to control the parents' actions or isolate them from family and friends. When hiring a professional caregiver, be sure to check their resume and references and pay for a professional credit and background check. Finally, note that more than half of all instances of caregiver fraud are committed by a family member.

Finally, children might want to get involved with managing their parents' money. Although this can be a delicate topic to suggest, keeping an eye on things can aid in noticing trouble early. Even simply looking over their phone bills or financial statements can uncover large ATM withdrawals or expensive calls to 900 numbers.”

If you suspect a parent or other aging family member or friend might be a victim in financial exploitation, there are ways to help. Contacting a financial advisor or counselor and getting them involved is a good way to provide expertise in a delicate and serious situation for your loved one.

As always, I am available and welcome your questions or comments. Feel free to email us by clicking here.

Senior financial abuse doesn't seem to make headlines on CNN, but it is very prevalent. I was surprised to see some of these statistics in a recent survey done by these organizations: the North American Securities Administrators Association (NASAA), Investor Protection Trust, and the National Adult Protective Services Association (NAPSA).

Here are some surprising statistics from their survey:

• Half of older Americans exhibit one or more of the warning signs of current financial victimization.

• Almost half of those aged 65 or over (44 percent) got at least two out of four questions wrong about basic investment knowledge.

• About one out of three older Americans (31 percent) says they are vulnerable in one or more ways to potential financial victimization.

• Only 5 percent of adult children in touch with their parents' doctors report "the healthcare providers ever mention[ing] any concerns about your parents handling of money or relayed any concern from your parent about handling money." Only 2 percent of Americans aged 65 or older say that their healthcare provider has ever asked about "how you are handling money issues or problems."

• Four out of 10 children of parents 65 or older are "very" or "somewhat" worried that their parents "have already become or will become less able to handle their personal finances over time."

Half of our seniors exhibit warning signs of financial exploitation? Sounds scary, doesn't it? I am relieved that there are some who have heeded the warning signs and are taking action. The NASAA, Investor Protection Trust, and the NAPSA, along with medical professionals and social workers, are banning together to create the Elder Investment Fraud and Financial Exploitation project, whose sole job is to stop a "rising tide of economic exploitation of the elderly." (Kristof, LA Times)

But what can the average person do right now to prevent senior financial exploitation? The California Society of CPA's recommends that the best defense is a good offense:

• Be aware – it can happen to your family

• Identify vulnerabilities

• Take action to safeguard your family

• Look for clues of abuse

• Take action if you suspect fraud

Sheryl Rowling of Advisors4Advisors further explains what that action can look like:

“Financial fraud can occur in small amounts over time. For seniors on a fixed income, even $10 here and $20 there can be devastating. The most common scams against seniors fall into three groups:

• Telemarketing scams: More than a third of telemarketing fraud victims are over 60 years old. The most common scams are free vacations packages, time shares, sweepstakes, phony charity fund raisers, and expensive 900 numbers.

• "Free" lunch investment seminars: Shady financial advisers often lure seniors to a free lunch or dinner, promising advice on “senior” issues such as living trusts or estate planning. Once there, seniors are pressured into purchasing dubious investments such as annuities or promissory notes. Although technically legal, these products are monumentally bad choices for retirees - illiquid, complicated and booby-trapped with high fees.

• Religious or social group fraud: Among con artists' favorite targets are members close knit religious or social groups. The con joins the group and then tries to sell fraudulent investment schemes to members.

One of the easiest - and most effective - ways to protect parents is to talk to them about the common financial scams. Tell them it's important they know what's happening - if for no other reason than to warn their friends.

Also, it's important that children know their parents' social circle. Are they mentioning a new name? Have they begun to talk about someone that has "a lot of good ideas" about money? Children should introduce themselves to new people entering their parents' life. Con artists are looking for easy marks, not people with family or friends looking out for them.

Theft committed by a caregiver, such as a nurse or aide, can be very difficult to uncover. There are warning signs of caregiver financial abuse. Watch for signs that a caregiver is trying to control the parents' actions or isolate them from family and friends. When hiring a professional caregiver, be sure to check their resume and references and pay for a professional credit and background check. Finally, note that more than half of all instances of caregiver fraud are committed by a family member.

Finally, children might want to get involved with managing their parents' money. Although this can be a delicate topic to suggest, keeping an eye on things can aid in noticing trouble early. Even simply looking over their phone bills or financial statements can uncover large ATM withdrawals or expensive calls to 900 numbers.”

If you suspect a parent or other aging family member or friend might be a victim in financial exploitation, there are ways to help. Contacting a financial advisor or counselor and getting them involved is a good way to provide expertise in a delicate and serious situation for your loved one.

As always, I am available and welcome your questions or comments. Feel free to email us by clicking here.

Bookmark this post: |

|

Monday, June 14, 2010

What is a Fiduciary? And why is it Important to You?

The fiduciary standard is a code of conduct for registered investment advisors who are regulated under the Investment Advisors Act of 1940. I am a registered investment advisor so therefore I am held to the fiduciary code of conduct. This important standard requires me to:

Brokers are not required to show conflicts of interest, details of his/her fee structure (which would be pretty shocking if disclosed) or to make sure that the product being sold or offered to the client is truly best for that client. And if a client is wronged by a broker, the burden of proof is on the client to show the damage. As a fiduciary, the burden on proof is for me to show that I am right or wrong.

So...who would you trust to manage your portfolio, make recommendations, help you to retire etc....? A broker or a true fiduciary who sits on the same side of the table as you!

The House-Senate Conference Committee is grappling with this issue right now and deciding whether all financial advisors should be held to the fiduciary standard. This is a no-brainer, in my opinion. We all should be fiduciaries. The brokerage and insurance industries are working hard to strike the fiduciary provision from the reform bill.

Let your voice be heard. Contact the committee members today and let them know that a Fiduciary Standard is the best thing we can do for financial reform.

- always put your interest first

- act with prudence

- never mislead you

- provide full disclosure

- avoid conflicts of interest

- and fully disclose and fairly manage (in your interest) any unavoidable conflicts.

Brokers are not required to show conflicts of interest, details of his/her fee structure (which would be pretty shocking if disclosed) or to make sure that the product being sold or offered to the client is truly best for that client. And if a client is wronged by a broker, the burden of proof is on the client to show the damage. As a fiduciary, the burden on proof is for me to show that I am right or wrong.

So...who would you trust to manage your portfolio, make recommendations, help you to retire etc....? A broker or a true fiduciary who sits on the same side of the table as you!

The House-Senate Conference Committee is grappling with this issue right now and deciding whether all financial advisors should be held to the fiduciary standard. This is a no-brainer, in my opinion. We all should be fiduciaries. The brokerage and insurance industries are working hard to strike the fiduciary provision from the reform bill.

Let your voice be heard. Contact the committee members today and let them know that a Fiduciary Standard is the best thing we can do for financial reform.

Bookmark this post: |

|

Tuesday, June 8, 2010

Stewart Financial Services News

We're excited to share this new communication tool with all of our friends and clients!

Sincerely,

Judy, Cheryl and Marcie

Bookmark this post: |

|

Monday, June 7, 2010

SmartyPig

Hi everyone, this is Marcie here guest blogging today. Part of my position here at Stewart Financial Services is connecting new technology and social media trends with the sector of finance and financial planning. We are always on the look out for innovative ideas to find holistic and safe finance advice, relationships, and technology that our clients can use.

Today, I wanted to talk about a really neat organization we found that utilizes social media, teaches good saving practices, and is a safe institution to use (and free!). It's called SmartyPig.

SmartyPig is a organization that allows anyone to open up a savings account for free. Straight from their FAQ page: SmartyPig is a unique savings program that was designed to help people save for specific goals. Goals may be funded with a monthly recurring contribution from your existing checking or savings account. You can also make one-time additions of money toward your goals and receive contributions from your friends and family members.

SmartyPig is a organization that allows anyone to open up a savings account for free. Straight from their FAQ page: SmartyPig is a unique savings program that was designed to help people save for specific goals. Goals may be funded with a monthly recurring contribution from your existing checking or savings account. You can also make one-time additions of money toward your goals and receive contributions from your friends and family members.

What's great about this is that it's, wait for it... FREE. There are no monthly fees. Every account is FDIC insured for balances under $250,000. The initial deposit is only $25.00 and account holders earn 2.15% APY on balances under $50,000, which American Consumer News states, "one of the best rates available for FDIC insured savings accounts."

You can also use social media applications like Facebook and Twitter to help your family and friends fund your stated savings goal. Tired of receiving shirts from Aunt Susan that you don't like? A simple fix is sending Aunt Susan a link to your SmartyPig account and let her deposit the money into your account for your stated goal. Goals can be anything you want: a trip, a shopping spree, or a night on the town. Plus, if you use one of their retail partners, you can boost your money by up to 12%: places like Amazon.com, Macy's, or Travelocity.

As great as SmartyPig is for adults (and for me, I signed up to fund a trip to Hawaii), this is a great tool teaching children how to save. American Consumer News blogs about how to use SmartyPig as a tool to teach children how to save:

"Watching a saving account grow via compound interest can help teach a child the importance and benefits of savings and investing at an early age.

Perhaps the most important lesson that your child will learn with a SmartyPig account is the power of setting and achieving goals. They will see the direct correlation between the amount of effort that they put in and the results of their success."

For accounts for children under 18, SmartyPig says this, "Anyone may have a SmartyPig account. But customers under 18 years of age must be invited to become co-owners by parents or legal guardians who have first opened their own SmartyPig accounts."

To test out SmartyPig, I went ahead and opened an account. Here's a list of things I needed to begin:

I found setting up an account easy and intuitive. After 10 minutes, I had validated my information, set up my security questions and answers, and finished registration with a working account. The next step is setting up routing and bank information in which you want to transfer from. Remember: your first transfer only has to be $25.00 and $10.00 monthly after that.

And, dare I say that setting up an account with my goal was actually fun?! Now instead of getting that t-shirt from Aunt Susan, all I need to do is to send my link around for my birthday and imagine sitting in Hawaii two years from now. Yeah!

If you have any questions about this post, saving accounts, or any other things, feel free to contact Stewart Financial Services at our email or give us a call at 888.891.9709. We'd be happy to help. Happy Saving!

Today, I wanted to talk about a really neat organization we found that utilizes social media, teaches good saving practices, and is a safe institution to use (and free!). It's called SmartyPig.

What's great about this is that it's, wait for it... FREE. There are no monthly fees. Every account is FDIC insured for balances under $250,000. The initial deposit is only $25.00 and account holders earn 2.15% APY on balances under $50,000, which American Consumer News states, "one of the best rates available for FDIC insured savings accounts."

You can also use social media applications like Facebook and Twitter to help your family and friends fund your stated savings goal. Tired of receiving shirts from Aunt Susan that you don't like? A simple fix is sending Aunt Susan a link to your SmartyPig account and let her deposit the money into your account for your stated goal. Goals can be anything you want: a trip, a shopping spree, or a night on the town. Plus, if you use one of their retail partners, you can boost your money by up to 12%: places like Amazon.com, Macy's, or Travelocity.

As great as SmartyPig is for adults (and for me, I signed up to fund a trip to Hawaii), this is a great tool teaching children how to save. American Consumer News blogs about how to use SmartyPig as a tool to teach children how to save:

"Watching a saving account grow via compound interest can help teach a child the importance and benefits of savings and investing at an early age.

Perhaps the most important lesson that your child will learn with a SmartyPig account is the power of setting and achieving goals. They will see the direct correlation between the amount of effort that they put in and the results of their success."

For accounts for children under 18, SmartyPig says this, "Anyone may have a SmartyPig account. But customers under 18 years of age must be invited to become co-owners by parents or legal guardians who have first opened their own SmartyPig accounts."

To test out SmartyPig, I went ahead and opened an account. Here's a list of things I needed to begin:

I found setting up an account easy and intuitive. After 10 minutes, I had validated my information, set up my security questions and answers, and finished registration with a working account. The next step is setting up routing and bank information in which you want to transfer from. Remember: your first transfer only has to be $25.00 and $10.00 monthly after that.

And, dare I say that setting up an account with my goal was actually fun?! Now instead of getting that t-shirt from Aunt Susan, all I need to do is to send my link around for my birthday and imagine sitting in Hawaii two years from now. Yeah!

If you have any questions about this post, saving accounts, or any other things, feel free to contact Stewart Financial Services at our email or give us a call at 888.891.9709. We'd be happy to help. Happy Saving!

Bookmark this post: |

|

Sunday, May 30, 2010

Memorial Day Remembrance

People always talk about "celebrating" Memorial Day. But when you really think about it, what is there to "celebrate"? Memorial Day is a day to remember and honor our military for all of the sacrifices they've made. Since the Revolutionary War, over 775,000 Americans have died serving our country with countless numbers being wounded. Over 50,000 U.S. Citizens are (were) classified as "Missing in Action". Over 600,000 have been Prisoners of War. I fail to see what there is to celebrate. This doesn't mean we can't remember and honor our fighting heroes (they're all heroes) together with family and friends. Go camping, have picnics and BBQ's, enjoy the freedoms our military has fought to preserve; just remember the real purpose of Memorial Day.

Bookmark this post: |

|

Thursday, May 20, 2010

Small Business Heath Care Tax Credit

This new tax credit is part of the recently signed Affordable Care Act (healthcare). It helps small businesses and small tax exempt organizations afford the cost of providing health care coverage for their employees.

Small businesses started receiving postcards from the IRS last month with details on this new tax credit. Here are the major points:

I have also provided a youtube link for a video that explains this credit in more detail: http://www.youtube.com/watch?v=85i1kzIG57k

Small businesses started receiving postcards from the IRS last month with details on this new tax credit. Here are the major points:

- Credit is worth up to 35% of the premium costs paid by a small business in 2010 thru 2013. In 2014, the credit is increased to 50%

- Credit phases out for small businesses with average wages between $25,000 and $50,000 and for firms with with the equivalent of between 10 and 25 full time (FTE) employees

- A qualifying employer must cover at least 50% of the cost of health care coverage

- A qualifying employer must have less than 25 (FTE) workers

I have also provided a youtube link for a video that explains this credit in more detail: http://www.youtube.com/watch?v=85i1kzIG57k

Bookmark this post: |

|

Tuesday, May 18, 2010

New Law Allows Tax-Free Health Coverage to Older Children

Changes made by the recently enacted Patient Protection and Affordable Care Act, provide tax-free health coverage for an employee's children who are under age 27. The change is effective March 30, 2010. These changes immediately allow employers with cafeteria plans to permit employees to begin making pre-tax contributions to pay for this expanded benefit.

In addition to extending coverage to older children, the Affordable Care Act also requires plans that provide dependent coverage to continue to make the coverage available for an adult child until the child turns age 26. The extended coverage must be provided no later than plan years beginning on or after September 23, 2010. The favorable tax treatment applies to that extended coverage.

In addition to extending coverage to older children, the Affordable Care Act also requires plans that provide dependent coverage to continue to make the coverage available for an adult child until the child turns age 26. The extended coverage must be provided no later than plan years beginning on or after September 23, 2010. The favorable tax treatment applies to that extended coverage.

Bookmark this post: |

|

Thursday, May 13, 2010

COBRA Premium Subsidy extended for 3rd time

Congress has extended eligibility for the COBRA premium subsidy for two months as one provision of The Continuing Extension Act of 2010 enacted April 15th.

The subsidy, which expired March 31, is now available to qualified individuals who lost their jobs between September 1, 2008, and May 31, 2010. The premium reduction, originally a provision of The American Recovery and Reinvestment Act (ARRA), applies to periods of health coverage that began on or after February 17, 2009, and lasts for up to 15 months.

The subsidy already has been extended twice. Democrats in Congress are working on a bill that will extend the COBRA subsidy for a longer period, at least until the end of the year, but passage may prove difficult because of cost concerns.

Eligible individuals pay only 35 percent of their COBRA premiums and the remaining 65 percent is reimbursed to the coverage provider through a tax credit.

To be eligible for the subsidy, the terminated worker must have experienced a qualifying event, which can include a reduction in hours followed by termination; must elect the coverage within the required timeframe; and must not be eligible for Medicare or any other group coverage.

The premium subsidy is retroactive and will be made available to individuals who lost their job between March 31st and April 15th.

The subsidy, which expired March 31, is now available to qualified individuals who lost their jobs between September 1, 2008, and May 31, 2010. The premium reduction, originally a provision of The American Recovery and Reinvestment Act (ARRA), applies to periods of health coverage that began on or after February 17, 2009, and lasts for up to 15 months.

The subsidy already has been extended twice. Democrats in Congress are working on a bill that will extend the COBRA subsidy for a longer period, at least until the end of the year, but passage may prove difficult because of cost concerns.

Eligible individuals pay only 35 percent of their COBRA premiums and the remaining 65 percent is reimbursed to the coverage provider through a tax credit.

To be eligible for the subsidy, the terminated worker must have experienced a qualifying event, which can include a reduction in hours followed by termination; must elect the coverage within the required timeframe; and must not be eligible for Medicare or any other group coverage.

The premium subsidy is retroactive and will be made available to individuals who lost their job between March 31st and April 15th.

Bookmark this post: |

|

Monday, May 10, 2010

Is a Reverse Mortgage in Your Future?

Reverse mortgages are a curious and complex topic. There is a lot of misunderstanding and confusion about them. They have received bad press and good press. So, let's try and demystify them and see if they make sense for you.

Using a reverse mortgage may make sense for a lot of baby boomers who will not have sufficient retirement savings when they finally retire. And with the uncertainly over Social Security and the compelling arguments that benefits will most likely change in the next few years, a reverse mortgage may be the product that allows boomers to have a comfortable retirement.

For some folks, the only true valuable asset may be their home with a low mortgage or no mortgage. A reverse mortgage converts your home equity into tax free proceeds and the owners retain title to their home. The reverse mortgage payments do not count towards Social Security and Medicare. The payments can cover living expenses, long term health care, home health care etc... It can be an important and necessary safety net for those folks with limited savings. Here are some facts about how a reverse mortgage works:

Using a reverse mortgage may make sense for a lot of baby boomers who will not have sufficient retirement savings when they finally retire. And with the uncertainly over Social Security and the compelling arguments that benefits will most likely change in the next few years, a reverse mortgage may be the product that allows boomers to have a comfortable retirement.

For some folks, the only true valuable asset may be their home with a low mortgage or no mortgage. A reverse mortgage converts your home equity into tax free proceeds and the owners retain title to their home. The reverse mortgage payments do not count towards Social Security and Medicare. The payments can cover living expenses, long term health care, home health care etc... It can be an important and necessary safety net for those folks with limited savings. Here are some facts about how a reverse mortgage works:

- Qualifying is not dependent on income, health, employment or credit score

- Only available for folks age 62 and over

- Must have a low mortgage balance or no mortgage balance

- Must attend a counseling session with a HUD approved agency so that you are fully informed of how a reverse mortgage works and also look at other options

- Can be taken as a lump sum, monthly annuity or line of credit

- Upon death, the beneficiaries will need to pay back the loan and the interest if they are keeping the house. If selling the house, all monies need to be paid back from the sale.

Please be aware the Reverse Mortgages are expensive--the fees are high. However, the benefits can be huge to folks who simply do not have enough funds to live a comfortable retirement.

In summary, a Reverse Mortgage can be a viable option in retirement in providing needed tax free income. Make sure that you do your homework and know all the ins and outs of how this works before entering into a binding contract.

Bookmark this post: |

|

Thursday, May 6, 2010

The Truth About Annuities

I have to admit up front that I am not a fan of annuities, except in very rare situations. The sad facts are that 90% of the folks who buy an annuity have absolutely no idea what they are buying and 90% of the folks who buy an annuity really don't need this investment product.

Annuities are a very lucrative product for insurance sales reps to sell. They typically receive 3 to 8% of the deposit money. So, let's assume that you deposit $100,000 in an annuity. The sales rep can receive up to $8000 for selling you this product! Pretty outrageous commissions.

An annuity is really an insurance contract. Many times the sales rep will tell you that the investment is insured against loss because when you die, your heirs will always receive at least the original value of the annuity insurance contract. So, you are paying a steep fee for this insurance protection. However, with most conservative investments, over time, your investment should at least be worth what you started with. So, the extra cost for the insurance is expensive and not needed.

Annuities carry heavy surrender charges. If you need your money in the first 7 to 10 years after opening the annuity, you most likely will pay anywhere from 7-10% in surrender charges. On your own money!

Annuities are often sold as "safe investments". But remember that insurance companies can fail and investments can go south. Nothing is guaranteed. Especially in this economy where we have witnessed huge companies going bankrupt in the past few years. Did you ever think GM would need to be rescued?

Annuities are sold to folks for "tax savings". This is because the money inside an annuity grows tax deferred. However, once the money starts to get distributed (either to the person who bought the annuity or the heirs) the distributions are taxed at the highest rate. All distributions are treated as ordinary income. If you held this money in a taxable brokerage account, you would pay capital gains rate on the earnings and not ordinary income tax rates. Big difference.

Annuities typically have very limited investment options. Most offer high cost captive mutual funds with few good choices.

Annuities should never be purchased within an IRA account. IRAs are tax deferred already so it makes no sense to put a tax deferred annuity in an already tax deferred account. Remember...big commissions on the sales of annuities!

And finally...annuities are hardly ever "bought"...they are almost always "sold".

Annuities are a very lucrative product for insurance sales reps to sell. They typically receive 3 to 8% of the deposit money. So, let's assume that you deposit $100,000 in an annuity. The sales rep can receive up to $8000 for selling you this product! Pretty outrageous commissions.

An annuity is really an insurance contract. Many times the sales rep will tell you that the investment is insured against loss because when you die, your heirs will always receive at least the original value of the annuity insurance contract. So, you are paying a steep fee for this insurance protection. However, with most conservative investments, over time, your investment should at least be worth what you started with. So, the extra cost for the insurance is expensive and not needed.

Annuities carry heavy surrender charges. If you need your money in the first 7 to 10 years after opening the annuity, you most likely will pay anywhere from 7-10% in surrender charges. On your own money!

Annuities are often sold as "safe investments". But remember that insurance companies can fail and investments can go south. Nothing is guaranteed. Especially in this economy where we have witnessed huge companies going bankrupt in the past few years. Did you ever think GM would need to be rescued?

Annuities are sold to folks for "tax savings". This is because the money inside an annuity grows tax deferred. However, once the money starts to get distributed (either to the person who bought the annuity or the heirs) the distributions are taxed at the highest rate. All distributions are treated as ordinary income. If you held this money in a taxable brokerage account, you would pay capital gains rate on the earnings and not ordinary income tax rates. Big difference.

Annuities typically have very limited investment options. Most offer high cost captive mutual funds with few good choices.

Annuities should never be purchased within an IRA account. IRAs are tax deferred already so it makes no sense to put a tax deferred annuity in an already tax deferred account. Remember...big commissions on the sales of annuities!

And finally...annuities are hardly ever "bought"...they are almost always "sold".

Bookmark this post: |

|

Tuesday, May 4, 2010

California and the new tax credits

California is offering some nice tax credits for folks who buy either a new home (never been occupied) or a first home. These credits are available for purchases that close escrow on or after May 1, 2010. Here are the rest of the details:

- Applications for the credit must be faxed after escrow closes

- Credits are available for taxpayers who purchase a qualified personal residence only after May 1, 2010 and before January 1, 2011

- Tax credits limited to the lesser of 5% of the purchase price or $10,000, whichever is smaller

- Tax credit received over a 3 year period ($3333 per year) beginning with the tax year the home is purchased.

- Tax credits are non refundable and unused credits cannot be carried over

For both the First Time Home buyer and the New Home Buyer credits, the taxpayer must live in the home for 2 years following the close of escrow.

California has allocated $100 million for the New Home credit and $100,000 for the First Time Buyer credit. Credits allocated on a first come, first served basis. We expect the credits to go fast so if you know of someone who qualifies under the rules, let them know ASAP.

Bookmark this post: |

|

Thursday, April 29, 2010

What To Do When Your Home Is Underwater

Currently, there is so much consternation for consumers concerning their homes right now. This article written by a colleague of mine really details the options that are available and the ramifications of each one. Very good article.

Here is a link to the blog by Burt Whitehead, "What To Do When Your Home Is Underwater."

Here is a link to the blog by Burt Whitehead, "What To Do When Your Home Is Underwater."

Bookmark this post: |

|

Sunday, April 11, 2010

Inflation or Deflation???

Excellent article written by some of my colleagues at Cambridge Advisors. Enjoy reading.

Bert Whitehead's blog about Inflation or Deflation

Bert Whitehead's blog about Inflation or Deflation

Bookmark this post: |

|

Monday, March 29, 2010

Long Term Care Benefits

Something interesting that is part of the Health Reform Act.

Long-term Care Benefit Also Made Available in Health Reform

March 26, 2010 (PLANSPONSOR.com) - The health reform legislation contains a provision that will make long-term care insurance available to all Americans, who will be automatically enrolled with the choice to opt out.

Under the Community Living Assistance Services and Support (CLASS) Act, individuals will begin paying a premium immediately and, after five years, those with functional limitations have the option of receiving a cash benefit of around $50 a day that can be used for medical equipment and home renovations.

In addition, Health Leaders Media reports that the bill will implement much stricter guidelines in terms of ownership transparency of nursing home chains.

"This will allow patients and the public at large to better understand ownership and operational hierarchies that currently are difficult to identify. Making these changes in the industry will be challenging, particularly for large publically-owned chains," says Katherine McCarthy, business account manager at PointRight in Lexington, MA, according to the news report. "However, those of us in the industry are all very excited that the bill will extend the therapy caps exceptions process through 2010. At the end of this year, they will have to revisit this issue again, at which point we are all hopeful for a long-term fix that ensures patients are able to receive the care they need based on medical necessity, rather than an arbitrary cap on funding." The health reform bill also includes a provision to help close the Medicare Part D coverage gap for medications. According to the Senate’s summary of the Patient Protection and Affordable Care Act, "in order to have their drugs covered under the Medicare Part D program, drug manufacturers will provide a 50% discount to Part D beneficiaries for brand-name drugs and biologics purchased during the coverage gap beginning July 1, 2010. The initial coverage limit in the standard Part D benefit will be expanded by $500 for 2010."-Rebecca Moore

Long-term Care Benefit Also Made Available in Health Reform

March 26, 2010 (PLANSPONSOR.com) - The health reform legislation contains a provision that will make long-term care insurance available to all Americans, who will be automatically enrolled with the choice to opt out.

Under the Community Living Assistance Services and Support (CLASS) Act, individuals will begin paying a premium immediately and, after five years, those with functional limitations have the option of receiving a cash benefit of around $50 a day that can be used for medical equipment and home renovations.

In addition, Health Leaders Media reports that the bill will implement much stricter guidelines in terms of ownership transparency of nursing home chains.

"This will allow patients and the public at large to better understand ownership and operational hierarchies that currently are difficult to identify. Making these changes in the industry will be challenging, particularly for large publically-owned chains," says Katherine McCarthy, business account manager at PointRight in Lexington, MA, according to the news report. "However, those of us in the industry are all very excited that the bill will extend the therapy caps exceptions process through 2010. At the end of this year, they will have to revisit this issue again, at which point we are all hopeful for a long-term fix that ensures patients are able to receive the care they need based on medical necessity, rather than an arbitrary cap on funding." The health reform bill also includes a provision to help close the Medicare Part D coverage gap for medications. According to the Senate’s summary of the Patient Protection and Affordable Care Act, "in order to have their drugs covered under the Medicare Part D program, drug manufacturers will provide a 50% discount to Part D beneficiaries for brand-name drugs and biologics purchased during the coverage gap beginning July 1, 2010. The initial coverage limit in the standard Part D benefit will be expanded by $500 for 2010."-Rebecca Moore

Bookmark this post: |

|

Monday, March 1, 2010

Credit CARD Act of 2009

Last week, the most sweeping credit card reforms ever passed by Congress (The Credit CARD Act of 2009), began to take effect. On one side, consumer groups are excited that credit card companies are required to communicate more frequently and plainly about changes they make to your cards. Critics, however, say that these new regulations will make credit cards more expensive, in the long run, for everyone.

NPR’s “All Things Considered” outlines a few need-to-know-points for consumers:

— Payments and Billing: The issuer has to set the payment-due deadline on the same day each month.

— Fees: Consumers cannot be charged extra fees for making payments online, by phone or by mail.

— Disclosures: Issuers must notify cardholders of significant changes to their account terms at least 45 days before the changes take effect. If the consumer objects to the changes, he or she can close the account, or "opt out."

— Young People: Consumers younger than 21 need an adult co-signer to open a credit card. In addition, the card issuers cannot entice students to sign up by offering free pizzas or other gifts within 1,000 feet of a college campus.

Also, have you ever tried paying your credit card over the phone, only to realize it will cost you 10 bucks to do so? That’s also out with these new credit regulations. (They always try to nickel and dime us, don’t they?)

Bookmark this post: |

|

Monday, February 22, 2010

Why Your Credit Score is so Important

Your Credit Score is like your reputation, it follows you everywhere. Protect it as best as you can.

What Makes Up a Credit Score

A credit score takes into account a lot of different information from your credit report, but it’s not all treated equally. Some aspects of your credit history are more important than others and will weigh more heavily on your overall score. Your FICO score is essentially made up of the following:

· Payment History – 35%

· Total Amounts Owed – 30%

· Length of Credit History – 15%

· New Credit – 10%

· Type of Credit in Use – 10%

As you can see, the bulk of your credit score comes from your payment history and how much debt you actually have. Those two items account for 65% of your score. So, if you’re really looking to improve your credit score, these are the areas you’ll want to tackle first.

Why Your FICO Credit Score is Important

We’ve determined what makes up a credit score, but why is it so important? Your credit score will follow you for your entire life and if you are ever trying to borrow money, the lender is going to look at your credit score to determine whether or not to lend money to you. Need to buy a car? They will check your credit score. Looking for a mortgage? You can bet they are checking your credit score. In fact, even some employers are checking credit scores when hiring to possibly determine who would make a good employee.

Not only does your credit score determine whether or not you’ll receive financing, it also determines how much it will cost you to borrow that money. People with higher credit scores are deemed to be less of a risk and therefore will typically receive the lowest interest rates. Those with lower scores are viewed as more of a risk so the bank will offset that risk by lending you money at a higher interest rate. And when you’re talking about larger loans such as buying a vehicle or a home, just an extra interest rate point could add up to thousands, and even tens of thousands of dollars wasted on interest.

What Makes Up a Credit Score

A credit score takes into account a lot of different information from your credit report, but it’s not all treated equally. Some aspects of your credit history are more important than others and will weigh more heavily on your overall score. Your FICO score is essentially made up of the following:

· Payment History – 35%

· Total Amounts Owed – 30%

· Length of Credit History – 15%

· New Credit – 10%

· Type of Credit in Use – 10%

As you can see, the bulk of your credit score comes from your payment history and how much debt you actually have. Those two items account for 65% of your score. So, if you’re really looking to improve your credit score, these are the areas you’ll want to tackle first.

Why Your FICO Credit Score is Important

We’ve determined what makes up a credit score, but why is it so important? Your credit score will follow you for your entire life and if you are ever trying to borrow money, the lender is going to look at your credit score to determine whether or not to lend money to you. Need to buy a car? They will check your credit score. Looking for a mortgage? You can bet they are checking your credit score. In fact, even some employers are checking credit scores when hiring to possibly determine who would make a good employee.

Not only does your credit score determine whether or not you’ll receive financing, it also determines how much it will cost you to borrow that money. People with higher credit scores are deemed to be less of a risk and therefore will typically receive the lowest interest rates. Those with lower scores are viewed as more of a risk so the bank will offset that risk by lending you money at a higher interest rate. And when you’re talking about larger loans such as buying a vehicle or a home, just an extra interest rate point could add up to thousands, and even tens of thousands of dollars wasted on interest.

Bookmark this post: |

|

Monday, February 15, 2010

2010 Five Star Wealth Managers

A big thanks to San Diego Magazine and San Diego for honoring me and our practice this month. I am humbled and grateful for the honor of being one of San Diego Magazine's 2010 Five Star Wealth Managers.

A big thanks to San Diego Magazine and San Diego for honoring me and our practice this month. I am humbled and grateful for the honor of being one of San Diego Magazine's 2010 Five Star Wealth Managers. From February's San Diego Magazine, the award, "represents less than 4 percent of the wealth managers in the San Diego area. Only 456 of the top-scoring wealth managers made this year's list."

Cheryl, Marcie, and myself work hard to provide the best customer service and financial planning to all our clients. I am excited to share this honor with them and all our clients whom we serve.

Bookmark this post: |

|

Monday, January 25, 2010

Why You Should Convert to a Roth IRA in 2010

2010 offers us some special and unique planning opportunities. It allows all taxpayers to convert IRA (tax deferred) money to Roth IRAs (tax free money) regardless of adjusted gross income. In the prior years, only taxpayers with adjusted gross income of less than $100,000 were allowed to convert IRA money to a Roth IRA.

When a taxpayer converts money from a regular IRA to a Roth IRA there is a tax bill due. The taxes are based on the amount of conversion and taxed at the taxpayer’s current tax bracket. In other words, if $10,000 of regular IRA money is converted to a Roth and the taxpayer is in a 15% tax bracket, then $1500 of federal taxes would be owed in addition to state taxes.

2010 also offers another special situation in that the federal taxes owed for conversions in 2010 can be spread over 2 years rather than all being paid in one year. So, if we look at the same example above, the $1500 in taxes could be paid in 4/15/11 and 4/15/12. However, please note that if the tax brackets are higher in the later years, you will pay more in taxes. So, if you believe that we will see higher taxes down the road, it might make more sense to pay the entire tax bill in 4/15/11!

The entire IRA does not need to be converted. So, if a taxpayer has a $100,000 IRA but does not want to convert the entire IRA because of the high tax bill, he /she can convert just a portion of the IRA. And pay taxes only on the converted amount.

If there are non deductible contributions in the IRA account mixed in with deductible contributions, you cannot just convert the non deductible amounts. It must be pro-rated. Assume that a taxpayer has a $100,000 IRA and $40,000 is from non deductible or post tax contributions, then only 40% is non taxable if the entire IRA is converted. The other $60,000 would be taxable. If the same taxpayer decided to just convert $50,000, then $20,000 (40%) would be non taxable and $30,000 would be taxable.

And the final good news sounds like a TV commercial “if for any reason you are not satisfied, you can undo your Roth conversion absolutely free, with no further obligation”. It’s called a recharacterization and if you convert this year you have until 10/15/2011 to undo the conversion. For example, assume you convert $100,000 in 2010 and the market totally tanks and you end up with only $80,000 in your Roth but will owe taxes on the $100,000 that you converted. You can do a recharacterization and put the money back into your IRA and undo the whole transaction. Sounds almost too good to be true!

The earlier that you convert, the better off you will be. Consider that, over time, stocks have risen more than they have fallen. All other things being equal, converting earlier means that the dollar amount of your conversion will be lower, thereby costing you less in taxes.

When a taxpayer converts money from a regular IRA to a Roth IRA there is a tax bill due. The taxes are based on the amount of conversion and taxed at the taxpayer’s current tax bracket. In other words, if $10,000 of regular IRA money is converted to a Roth and the taxpayer is in a 15% tax bracket, then $1500 of federal taxes would be owed in addition to state taxes.

2010 also offers another special situation in that the federal taxes owed for conversions in 2010 can be spread over 2 years rather than all being paid in one year. So, if we look at the same example above, the $1500 in taxes could be paid in 4/15/11 and 4/15/12. However, please note that if the tax brackets are higher in the later years, you will pay more in taxes. So, if you believe that we will see higher taxes down the road, it might make more sense to pay the entire tax bill in 4/15/11!

The entire IRA does not need to be converted. So, if a taxpayer has a $100,000 IRA but does not want to convert the entire IRA because of the high tax bill, he /she can convert just a portion of the IRA. And pay taxes only on the converted amount.

If there are non deductible contributions in the IRA account mixed in with deductible contributions, you cannot just convert the non deductible amounts. It must be pro-rated. Assume that a taxpayer has a $100,000 IRA and $40,000 is from non deductible or post tax contributions, then only 40% is non taxable if the entire IRA is converted. The other $60,000 would be taxable. If the same taxpayer decided to just convert $50,000, then $20,000 (40%) would be non taxable and $30,000 would be taxable.

And the final good news sounds like a TV commercial “if for any reason you are not satisfied, you can undo your Roth conversion absolutely free, with no further obligation”. It’s called a recharacterization and if you convert this year you have until 10/15/2011 to undo the conversion. For example, assume you convert $100,000 in 2010 and the market totally tanks and you end up with only $80,000 in your Roth but will owe taxes on the $100,000 that you converted. You can do a recharacterization and put the money back into your IRA and undo the whole transaction. Sounds almost too good to be true!

The earlier that you convert, the better off you will be. Consider that, over time, stocks have risen more than they have fallen. All other things being equal, converting earlier means that the dollar amount of your conversion will be lower, thereby costing you less in taxes.

Bookmark this post: |

|

Wednesday, January 20, 2010

Haiti Charitable Giving and 2009 Taxes

I am proud of our country and our citizens in how we as a nation have stepped up with our time, talent and financial resources to help the folks in Haiti. It has been very gratifying to see the outpouring of prayers and donations for this most impoverished country. Haiti's pain has truly captured the hearts of America and we have responded generously.

I am pleased to say that the House passed a bill yesterday that will allow all donations to Haiti Relief organizations to be considered charitable contributions on tax returns for 2009. Senate approval is expected as well. This applies to donations made after January 11th, 2010 and before March 1, 2010. Even though most of us give from our hearts and not because of tax reasons, it is nice to know that we get to reduce our 2009 taxes and help out Haiti as well.

If you are considering making a financial gift to Haiti, please do so by end of February and lower your 2009 taxes!

I am pleased to say that the House passed a bill yesterday that will allow all donations to Haiti Relief organizations to be considered charitable contributions on tax returns for 2009. Senate approval is expected as well. This applies to donations made after January 11th, 2010 and before March 1, 2010. Even though most of us give from our hearts and not because of tax reasons, it is nice to know that we get to reduce our 2009 taxes and help out Haiti as well.

If you are considering making a financial gift to Haiti, please do so by end of February and lower your 2009 taxes!

Bookmark this post: |

|

Subscribe to:

Posts (Atom)